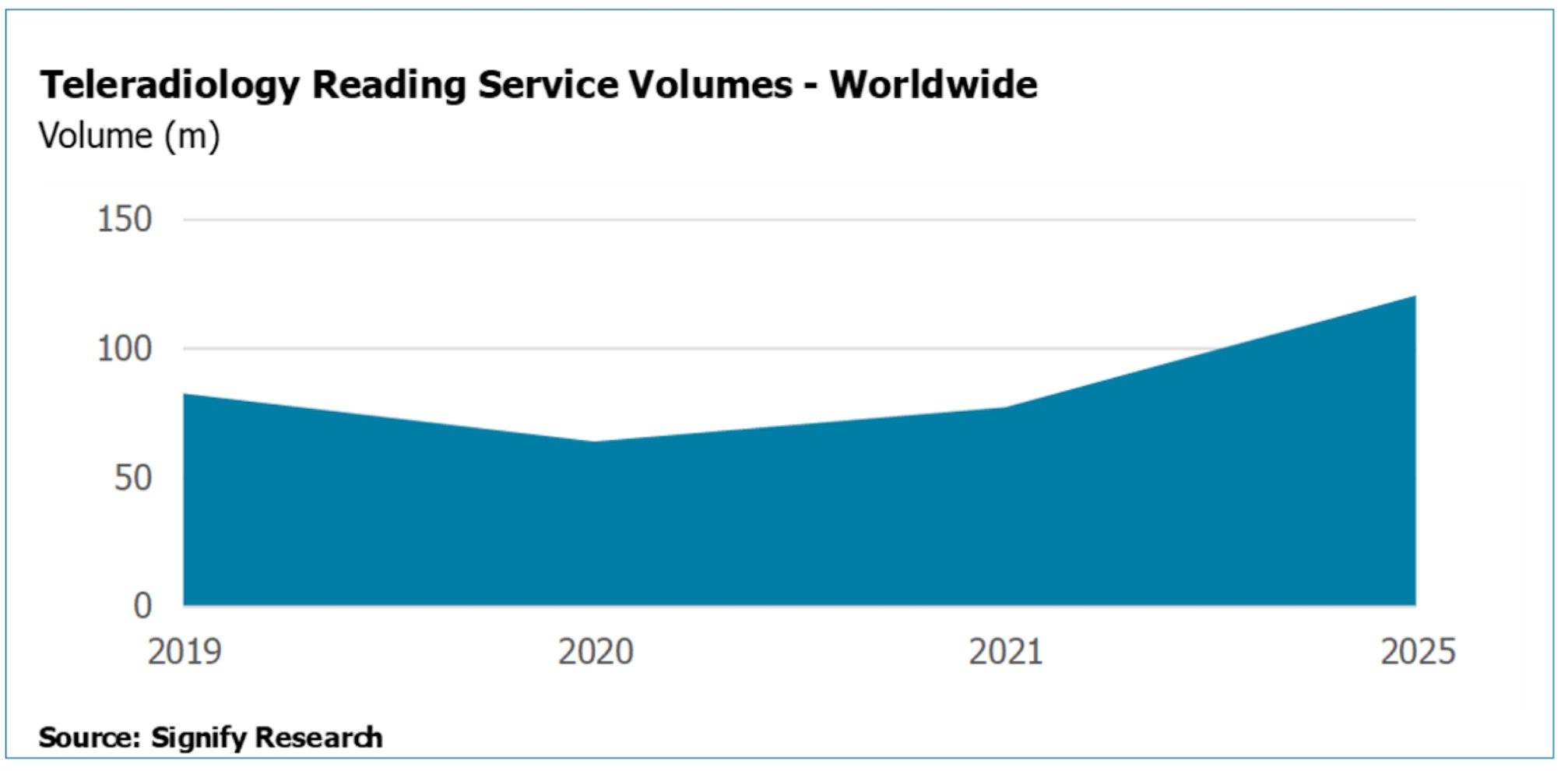

Outlook for 2021 and Beyond. As displayed in the figure below, these six market drivers are projected to result in teleradiology reading service volumes increasing by 21% in 2021 and nearly doubling by 2025. Revenues for teleradiology reading service providers are forecast to follow a similar profile over this period.

The closely tied relationship between teleradiology reading services and diagnostic imaging procedures resulted in an enormously challenging year for the teleradiology market. As healthcare providers’ resources became almost entirely focused on caring for those infected by the devastating COVID-19 virus, it contributed to the widespread global postponement of diagnostic imaging examinations. Considerably fewer imaging procedures performed led to hospitals, radiology groups and imaging center radiologists having more in-house capacity to interpret diagnostic images than they otherwise would have. The knock-on effect for the teleradiology market was a substantial drop off in demand for routine, non-emergency, daytime reporting, contributing to a 22 percent decline in overall 2020 reading service volumes.

But when will demand for teleradiology services return to pre-pandemic levels and what will drive the bounce back? Here we explore six key drivers that will reverse the trend seen in 2020.

1. National vaccination programs easing pressure on healthcare providers.

While many countries throughout the world have experienced a surge in cases of new COVID-19 variants in the first half of 2021, vaccination programs are progressing well in most developed countries and are likely to be in the latter stages (double dose) in late 2021, decreasing the likelihood of serious illness leading to patient hospitalizations or deaths. This will result in lower pressure on healthcare providers to provide care for critically ill patients and ultimately fewer postponements of non-emergent diagnostic imaging procedures.

2. Shortage of radiologists.

The supply of radiologists capable of interpreting more specialist and complicated diagnostic imaging procedures is falling, with financial constraints placed on public healthcare service providers limiting their ability to invest in trainee radiologists. The ability to retain and recruit radiologists is also proving a significant challenge for the industry. With the demand for diagnostic imaging procedures growing at a faster rate than the supply of radiologists, healthcare providers are increasingly becoming reliant on outsourcing their diagnostic reporting workload to teleradiology providers.

3. Increased requirement for specialized modalities.

X-ray was the most popular modality in 2020 and accounted for 60 percent of worldwide diagnostic imaging volumes. Despite the preference to use X-ray for the diagnosis of COVID-19 patients in western geographies (such as the U.S. and U.K.), its share of overall modality volumes fell in 2020, partly due to the preference of computed tomography (CT) for COVID-19 diagnosis in Asian countries, particularly in China, the country performing the highest volume of diagnostic imaging procedures globally.

Demand for ultrasound, CT and magnetic resonance imaging (MRI) modalities are on course for significantly higher rates of growth than X-ray. This is due to the advantages of using specialist modalities, including greater detection and visibility of soft tissues, cancers and tumors. As demand for specialized modalities increases, so does the requirement for specialist radiologists capable of interpreting complicated imaging examinations. Where access to subspeciality expertise can be limited in-house (e.g. in smaller hospitals/radiology groups), teleradiologist expertise provides an ideal solution.

4. Huge backlog of diagnostic imaging procedures.

There is a huge backlog of elective procedures that were postponed during the pandemic; 2020 diagnostic imaging volumes were down by 18 percent, translating to almost one billion fewer procedures performed versus 2019. Many of these will require imaging from the more complex modalities, and therefore strong demand for teleradiology, which will be required to serve pent-up demand.

5. Demand for out-of-hours reporting.

The primary driver for out-of-hours reporting is for time-critical applications, such as neurology, or if there is suspicion of serious injury; these patients will require fast and accurate diagnosis. Out of hours reads are typically for treating hospital patients in intensive care or emergency rooms. The diagnostic image will be transmitted externally to a teleradiologist for reporting with a short turnaround time — within 30 minutes for preliminary read and 60 minutes for a final read — depending on the urgency. Emergency reads accounted for the majority of overnight work conducted by teleradiologists in 2020. The out of hours reporting function was verified as the primary driver of teleradiology reading services in 2020, as demand from healthcare providers remained relatively robust during the pandemic.

6. Healthcare providers focus on operational efficiency.

Healthcare providers globally are increasingly turning to teleradiology reading service providers in order to improve operational efficiency. In the U.S., the Centers for Medicare & Medicaid Services’ (CMS) December 2020 announcement to drastically cut diagnostic radiology reimbursement by 10 percent in 2021 will impact the U.S. diagnostic imaging market. To some extent reduced reimbursement rates may act as a market barrier and reduce the attractiveness of setting up a teleradiology reading service. However, the reimbursement cuts are expected to place further pressure on U.S. healthcare providers to downsize their internal workforce, drive consolidation of outpatient imaging centers and push to more outsourcing from hospitals, with an increased focus on operational efficiency; this is forecast to act as a market driver and stimulate additional demand for teleradiology and artificial intelligence (AI)-based solutions.

Arun Gill joined Signify Research in 2019 as part of the digital health team focusing on telehealth, PHM and EHR/EMR. He brings with him 10 years of experience as a senior market analyst.

Editor’s note: This analysis is a summary of data and commentary from Signify Research’s Teleradiology – World – 2021 market report. This report builds on the previous edition published in 2020 and provides an up-to-date assessment of the current status for diagnostic imaging procedures by modality, and the teleradiology reading services and IT market. It explores the impact of COVID-19, specifically, in 20 core countries and sub-regions, and looks at when the market will begin to increase back to and beyond pre-pandemic levels. Forecasts are provided to 2025 for the market for teleradiology reading services (reading volumes, revenues and revenue per read), teleradiology IT and the competitive environment (from a reading service provider and IT vendor perspective) in each of the 20 countries and sub-regions mentioned above.

July 28, 2026

July 28, 2026